Part 4 of 4

III. The Trump Organization and Respondents Still Have Not Produced a Complete Set of Responsive Documents for Donald J. Trump321. As the Court is aware, there have been ongoing issues with the production of documents by the Trump Organization.

322. As a result of those delays, as of today, more than two years after the issuance of the initial subpoena to the Trump Organization, OAG still does not have a complete production of responsive custodial documents for Donald J. Trump.

323. Background information concerning the documentary subpoenas issued to the Trump Organization is laid out in the opening Verified Petition. See Docket No. 181 at ¶¶ 82- 126.

324. In the course of preparing for the testimony of Trump Organization counsel Jill Martin, OAG determined that certain documents—responsive to the subpoenas issued to the Trump Organization and containing search terms agreed to as part of the production process— had been produced by third parties but not the Trump Organization. Ex. 515. At that time, the Trump Organization had produced roughly 7,400 documents in total, substantially fewer than many third parties had produced.

325. By July 27, 2021, after conducting an audit of the production and taking four days of testimony from corporate representatives, OAG informed the Trump Organization that there were “number of serious failures in the Trump Organization’s subpoena responses.” Ex. 516.

326. Among the failures identified in that letter was the fact that the Trump Organization “appears to have produced only three custodial documents for Donald J. Trump, and these only in the last week.” Id. at 1. As set out in the letter:

5. The Trump Organization Produced Only Three Custodial Documents for Donald J. Trump

For more than 18 months, the Trump Organization failed to produce a single document held by its owner and former president Donald J. Trump -- despite the fact that the focus of the subpoena, and the investigation, is Mr. Trump's statement of financial condition. Mr. Trump personally executed documents central to the issues under investigation, like certifications of his statement of financial condition and conservation easements. Moreover, the statements on their face purport to contain valuations based on his evaluation. Mr. Garten testified that there were file cabinets at the Trump Organization holding Mr. Trump's files, that Mr. Trump had assistants who maintained files on his behalf, that he received and maintained hard copy documents, and that he used Post-It Notes to communicate with employees. It is impossible to take at face value the Trump Organization's conclusion that there was no reason to believe Mr. Trump was in possession of responsive information about his own personal financial statements, or that his custodial files lacked such information.

And that conclusion was proven false based on the July 22, 2021 production by the Trump Organization. Three documents in that production are flagged as being from the custodial files of Donald J. Trump.5 Each of the three documents is a personal letter from Mr. Trump to an executive of a financial institution expressly discussing and touting his statement of financial condition. For example, attached at Tab F is a letter from Mr. Trump to Richard Byrne, the CEO of Deutsche Bank Securities, dated November 2011 and enclosing his financial statement ("hopefully, you will be impressed!"), touting the prospects of the Doral property and enclosing a separate letter that "establishes my brand value, which is not included in my net worth statement." This document, as well as any other similar documents from Mr. Trump's individual files are of obvious relevance to the investigation and were plainly called for in the original subpoena.

Id. at 6.327. The Trump Organization offered no specific response to the point about the Donald J. Trump custodial files.

328. Following receipt of the letter, on August 27, 2021, the Trump Organization entered into an agreement with OAG tolling the statute of limitations for potential civil claims until October 31, 2021 with an option for OAG to extend the period to April 30, 2022 in its “sole discretion.” Ex. 517. OAG provided such notice extending the tolling agreement on September 28, 2021. Ex. 518.

329. In addition to the tolling agreement, after the July 27 letter, the Trump Organization agreed to enter into the Stipulated Order signed by this Court and docketed on September 3, 2021. Docket No. 314. Pursuant to the terms of that Order, the Trump Organization would undertake diligent efforts to comply with all outstanding subpoenas by October 15, 2021. After that date, if OAG reasonably determined that the Trump Organization had not met its obligation to comply with any outstanding subpoenas, the Trump Organization would retain an independent third-party e-discovery firm (“eDiscovery Firm”).

330. On November 1, 2021, OAG provided notice to the Trump Organization of the need to retain an eDiscovery Firm pursuant to the Stipulated Order. That letter highlighted again the failure to produce a set of custodial documents for Donald J. Trump:

1. The Trump Organization has not complied with its subpoena obligations

Although OAG's initial subpoena duces tecum was served in December 2019, productions from the Trump Organization only seem to have begun in earnest over the past two months; since the execution of a tolling agreement and entry of the Stipulated Order. During that time the Trump Organization has produced 751 ,035 documents which constitutes more than 97 percent of its total production of 769,813 documents. While OAG is still in the process of reviewing these documents, significant issues are already apparent. First, we still do not have a production of custodial documents for Donald J. Trump. Indeed, we have received no production of custodial documents for Mr. Trump since the production of the three letters from Mr. Trump on July 22, 2021, which we noted in our letter of July 27, 2021. All of this is despite testimony from the General Counsel Alan Garten that there were file cabinets at the Trump Organization holding Mr. Trump's files, that Mr. Trump had assistants who maintained files on his behalf, that he received and maintained hard copy documents, and that he used Post-It Notes to communicate with employees. Moreover, while the Trump Organization has interviewed 64 custodians to date, Rhona Graff is the only executive assistant to Donald J. Trump on that list. Attached at Tab A is a list of executive assistants at the Trump Organization and addresses for scanners and other imaging machines they used. At least five of those executive assistants worked for Donald J. Trump, nearly all of whom have sent documents to or on behalf of Mr. Trump.2 The failure to fully search these custodians and sources is a significant gap in compliance.

Ex. 519.331. The Trump Organization has offered no specific response to the point about the Donald J. Trump custodial files.

332. After initially objecting to the notice and a series of meet-and-confer discussions in advance of a potential court filing, on November 17, 2021 the Trump Organization agreed to retain an eDiscovery Firm. That eDiscovery Firm was formally retained on December 15, 2021. OAG has identified the custodial documents of Donald J. Trump as a priority item for the eDiscovery Firm.

333. Since the July 27 letter highlighting the discovery failures by the Trump Organization, the company has produced more than 900,000 documents. Of the roughly 933,000 documents produced in total, only three documents, produced on July 22, 2021, have metadata indicating they are the from the custodial files of Donald J. Trump. Productions continue to come in, with the most recent production on January 13, 2022, but there have been no further productions of documents tagged as Donald J. Trump custodial files since July 22, 2021.

334. The Trump Organization has provided more than a dozen weekly reports on the status of their ongoing production. None of those reports have addressed the custodial files of Donald J. Trump.

335. Indeed, Trump Organization productions appear lack even the most basic governing documents of the Donald J. Trump Revocable Trust—the trust entity that owns all or substantially all of the entities or assets comprising the Trump Organization apparently for Mr. Trump’s sole benefit and thus can be viewed as directing the operations of the Trump Organization. Some of what OAG has uncovered regarding this trust has been produced by third parties. For example, Donald J. Trump appears to have been the donor, sole trustee and sole beneficiary of the trust at one time. Ex. 520 (document dated January 4, 2017 and signed by Mr. Trump and reflecting certain transfers of interests). Mr. Trump then resigned as trustee, Ex. 521, and Allen Weisselberg and Donald Trump, Jr. accepted appointments as trustees effective January 19, 2017, Ex. 522. Documents also indicate significant transfers of Mr. Trump’s business interests to this trust. E.g., Ex. 523, Ex. 524.

336. But neither the Trump Organization nor Mr. Trump has produced a set of records, so far as OAG is aware, that comprehensively articulates how and under what rules this trust has operated. For example, the Trump Organization produced a document signed by Donald Trump, Jr. and Allen Weisselberg purporting to contain “true and correct portions of the Second Amendment of The Donald J. Trump Revocable Trust dated April 7, 2014” and including a document purporting to be such an amendment signed by Mr. Trump. Ex. 525. The attached amendment identifies Donald Trump, Jr. as “initial Trustee” and “Allen Weisselberg” as “initial Business Trustee.” Id. at -346. The amendment purports to be 34 pages long, but numerous pages plainly are missing, because the document is only eleven pages long and the document skips, for example, from “Page 2 of 34” to “Page 8 of 34.” Id. at -346, -347. The amendment articulates that “The trust shall be managed by my Trustees, including my Business Trustee (collectively, my “Trustees”), acting unanimously and in consultation with the Advisory Board, if any, subject to the limitations and requirements set forth therein.” Id. at -347. Eric F. Trump was identified as “initial Chairman of the Advisory Board” and empowered “in his sole discretion the number of members of the Advisory Board and the qualifications for membership.” Id.36

OAG SUBPOENAS TO RESPONDENTS, THEIR MOTION TO QUASH, AND THEIR FAILURE TO COMPLY WITH THE SUBPOENAS

I. Donald J. Trump Must Be Compelled to Testify and Produce Relevant Documents

A. Donald J. Trump must be compelled to testify about his misleading Statements of Financial Condition337. The financial statements under investigation purport to reflect his financial condition, purport to be his responsibility, and were the subject of certifications that he signed as to their truth and accuracy in connection with obtaining more than $300 million in loan proceeds (as well as other business transactions).

338. The financial statements under investigation are entitled, “Donald J. Trump Statement of Financial Condition.”37 They purport to reflect assets owned or controlled, directly or indirectly, by Donald J. Trump (or a revocable trust of which he is [sole] beneficiary)—and the statements are replete with contentions that the valuations presented are assessments made by, inter alia, Mr. Trump. See, e.g., Ex. 307 at PDF 14 (2009); Ex. 313 at MAZARS-NYAG- 0003139 (2011); Ex. 312 at MAZARS-NYAG-0000732 (2014).38 For example, the June 30, 2012 Statement of Financial Condition claims that Mr. Trump’s assets were identified at values “determined by Mr. Trump in conjunction with his associates and, in some instances, outside professionals” and asserts that a group of “club facilities and related real estate” was valued at more than $1.5 billion in an “assessment [that] was prepared by Mr. Trump working in conjunction with his associates and outside professionals.” Ex. 310 at MAZARS-NYAG- 00006313, -317. Moreover, in the years before Mr. Trump placed his assets into a revocable trust, the Statements of Financial Condition reflected that “Donald J. Trump is responsible for the preparation and fair presentation of the financial statement . . . .” Ex. 309 at MAZARSNYAG- 0003139 (2011) (emphasis added).

339. Furthermore, some evidence obtained by the Attorney General indicates that Mr. Trump was personally involved in reviewing and approving the Statements of Financial Condition before their issuance—a natural and logical focus of an investigation into whether a financial statement was fraudulent or misleading and, if so, who was responsible. Jeffrey McConney, Senior Vice President and Controller at the Trump Organization, appears to have been one of the principal participants in preparing the Statements of Financial Condition.39 When asked who reviewed these statements before they were finalized, he testified that his understanding was that “Allen Weisselberg I believe reviewed it with Mr. Trump,” that “Allen spoke with Mr. Trump about something with the statement,” and that “I guess we can assume” that Mr. Trump approved the statements before their issuance.40 Mr. McConney testified that he “wasn’t part of the conversations with Allen and Mr. Trump so I don’t know what they said.”41

340. Mr. Weisselberg, the Chief Financial Officer of the Trump Organization during the relevant period, similarly testified that it was “certainly possible” Mr. Trump discussed valuations with him and that it was “certainly possible” Mr. Trump reviewed the Statement of Financial Condition for a particular year before it was finalized.42 When pressed about whether Mr. Trump and he approved particular Statements of Financial Condition before their issuance, Mr. Weisselberg repeatedly invoked his Fifth Amendment privilege.43

341. Given the testimony of Mr. McConney and Mr. Weisselberg, Mr. Trump is the next logical subject of questioning regarding his participation in the creation of the Statements of Financial Condition and his approval of their contents.44

342. Mr. Trump also was personally involved in using the Statements of Financial Condition in numerous commercial transactions for his own financial benefit. Three loans issued by Deutsche Bank are cases in point. Mr. Trump’s personal guaranty in connection with that lender’s $125 million loan in connection with the Trump National Doral stated that Mr. Trump’s Statement of Financial Condition for a particular year was “true and correct in all material respects” and “presents fairly Guarantor’s financial condition.”45 Mr. Trump signed that guaranty.46 In the personal guaranty Mr. Trump signed in connection with the loan for the Old Post Office property, Mr. Trump stated that his Statement of Financial Condition for the year ending June 30, 2013 was “true and correct in all material respects” and “presents fairly [Mr. Trump’s] financial condition as of June 30, 2013.”47 Personal guaranties Mr. Trump signed in connection with the Chicago property reflected similar representations.48

343. Loan documents in connection with these loans also required Mr. Trump to annually deliver his Statement of Financial Condition for the ensuing years accompanied by a similar certification, and Mr. Trump in fact did so. For example, in a document dated November 11, 2014, Mr. Trump “hereby certifie[d]” that his Statement of Financial Condition for the year ending June 30, 2014 and other identified documents “presents fairly and accurately in all material respects the financial condition of Guarantor for the period presented.”49

344. Misrepresentations on such certifications and the Statements of Financial Condition to which they relate carried potentially serious consequences—even if only under the terms of these various loans. At origination, the truth of Mr. Trump’s representations was a condition precedent to the bank’s obligation to lend. Ex. 420 at DB-NYAG-005853, at 5911. In addition, an “event of default” would occur if “[a]ny representation or warranty of Borrower or Guarantor herein or in any other Loan Document” (including a compliance certificate) “shall prove to have been false or misleading in any material respect at the time made or intended to be effective.” Ex. 420 at DB-NYAG-005916.50

345. Mr. Trump also sent letters boasting to third parties about the contents of the Statements of Financial Condition—documents that are among the [extremely small] number of Mr. Trump’s custodial documents produced to NYAG to date.51

346. At the outset, Donald J. Trump offers no objection to that portion of his subpoena seeking the production of documents. To the contrary, on December 3, 2021, while leaving open the question of whether he would appear for testimony and objecting to the document return date of December 17, 2021, counsel for Mr. Trump agreed to produce responsive documents in advance of his testimony. At the same time, however, counsel indicated an understanding that all relevant documents were in the possession of the Trump Organization: “As I explained, I believe the documents you are seeking are in the possession of the Trump Organization and not in the possession of my client. We agreed that document production would not be addressed by the date of December 17. We will, of course, work on getting the documents you seek, if any, prior to his testimony.” Ex. 530.

347. To date, Mr. Trump has made no production of documents. Nor for that matter has the Trump Organization made anything approaching a complete production of documents for Mr. Trump. While Mr. Trump famously does not use email or a computer, he regularly generated handwritten documents.52 In testimony as a corporate representative, General Counsel Alan Garten testified that there were file cabinets at the Trump Organization holding Mr. Trump’s files, that Mr. Trump had assistants who maintained files on his behalf, that he received and maintained hard copy documents, and that he used Post-It Notes to communicate with employees.53 Yet as of June 30, 2021—more than 18 months after receiving the initial subpoena from OAG—the Trump Organization still had not searched for those documents. Indeed, Mr. Garten testified that, despite maintaining a “chron file” of correspondence for Mr. Trump, this file was never searched because the Trump Organization determined, improbably, that Mr. Trump was not involved in the preparation of his own financial statements. Ex. 531 at 317:18- 318:03 (“Q. Was the chron file searched for responsive information? A. No, because we did not believe he had any involvement in any of the areas that were the subject of the subpoenas. Q. How did you reach that conclusion? A. By interviewing other key witnesses and determining who was involved.”)

348. The Trump Organization reached this conclusion despite the representation in the financial statements that, “Donald J. Trump is responsible for the preparation and fair presentation of the financial statement in accordance with accounting principles generally accepted in the United States of America and for designing, implementing, and maintaining internal control relevant to the preparation and fair presentation of the financial statement.”54 The Trump Organization reached this conclusion despite testimony from Jeff McConney that Donald J. Trump would review and approve the financial statement with Allen Weisselberg.55

349. Less than a month later, the Trump Organization produced documents further demonstrating that its conclusion was unfounded. On July 22, 2021, the Trump Organization produced three letters from Mr. Trump, forwarding his financial statement an executive of a financial institution expressly discussing and touting his statement of financial condition.56 In one example, Mr. Trump wrote to Richard Byrne, the CEO of Deutsche Bank Securities, dated November 2011 and enclosing his financial statement (“hopefully, you will be impressed!”), touting the prospects of the Doral property and enclosing a separate letter that “establishes my brand value, which is not included in my net worth statement.”57 Metadata included with the production of those documents indicated that they were the custodial files of Donald J. Trump. But there have been no further productions of Mr. Trump’s custodial files since July 2021.

350. Beyond such direct correspondence about his financial statement, there are also documents concerning his involvement in the valuation of his property and the financial transactions that arose from those valuations. For example, Mr. Trump initialed and approved as “OK” an email from Allen Weisselberg providing for the Trump Organization to sign a 15 year master lease for retail space in 40 Wall Street as part of the refinancing of that property with Ladder Capital in 2015.58 Likewise, files from the Trump Organization reflect Mr. Trump’s signed and initialed certification attesting to certain aspects of his financial condition as part of the 2015 application to Ladder Capital.59

351. Yet neither Mr. Trump nor the Trump Organization have confirmed that an adequate search has been conducted, much less that all of his responsive documents have been produced. Both parties should be ordered to produce all responsive documents and certify to the completeness of that production within two weeks of a decision from this Court, and two weeks in advance of any testimony from Mr. Trump.

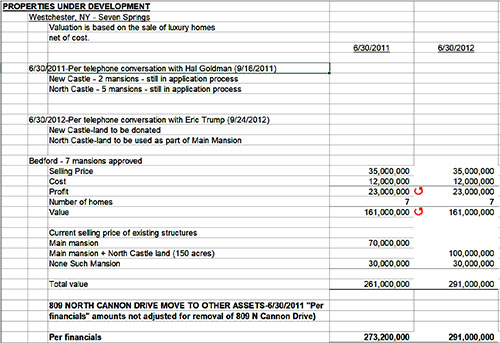

B. Donald J. Trump must be compelled to testify about the misleading appraisals he submitted to the Internal Revenue Service352. The Attorney General’s investigation likewise has obtained evidence indicating Mr. Trump’s intimate involvement in the development of the Seven Springs property. For example, one witness, who described his role as the “direct representative of Donald Trump” for counties including Westchester testified that Mr. Trump directed his activities, that he spoke to Mr. Trump personally about Seven Springs “[a]bout once a week,” and that he “seldom” communicated in writing with Mr. Trump because Mr. Trump indicated to him “that he did not want things put in writing in communications between us.”60 Mr. Trump has also publicly spoken about the development of the Seven Springs Property in a 2019 speech to the National Association of Realtors—stating that he that he fired a consultant who identified wetlands at the site:

But, you know, the environmental stuff was very tough. It was getting worse and worse every year. And I actually had this beautiful piece of land — 216 acres — and I was going to do something with it, and then I decided to do this. I’m glad I did this, because I can help more people. But, Tracy, they had a little area where water would sort of form when it rained. And all of a sudden, I found out that I can’t build on the land. Does that make sense to you? I can’t build on the land because it was considered, for all intents and purposes, a lake. And how did people find out about the lake? My consultant told them. Because, this way, you have to use your environmental consultant longer, pay them more money to get you out of the jam. Isn’t that nice? (Laughter.) I fired his ass so fast.

353. Matters related to the Seven Springs easement donation were reflected on Mr. Trump’s personal federal income tax returns for a series of years, which were produced to the Attorney General’s Office with Mr. Trump’s personal authorization. Moreover, the accounting firm that participated in preparing his tax returns has advised that conservation easements at Seven Springs and TNGC LA generated a federal tax benefit for Mr. Trump personally to the tune of more than $5 million over the course of tax years 2014 through 2018. The Attorney General’s Office obtained that concession only after Mr. Trump personally authorized his accounting firm to communicate it to this Office.

II. Donald Trump, Jr. Must Be Compelled to Testify354. Donald Trump, Jr.’s testimony similarly must be compelled because it similarly will bear a “reasonable relation” to matters under investigation by the Attorney General. Indeed, the Trump Organization (where Mr. Trump has been employed through much, if not all, of the relevant period) has already agreed that Donald Trump, Jr. is a custodian whose documentary evidence would be produced in response to the Attorney General’s subpoenas. There is no basis to deny the Attorney General the ability to examine Donald Trump, Jr. regarding that evidence and evidence OAG has received from other sources.

355. As set forth above, Donald Trump, Jr. is an Executive Vice President of the Trump Organization who manages the Trump Organization with Eric Trump. Evidence obtained by the Attorney General indicates that Donald Trump, Jr. was involved with certain Trump Organization properties that are valued on Mr. Trump’s Statement of Financial Condition, including 40 Wall Street, and was consulted in connection with the matters on the Statements of Financial Condition. Ex. 537 at CAPITALONE-00348338 (email sent to Donald Trump, Jr. providing him with the bank’s internal DCF projection of how the 40 Wall property will perform); Ex. 405 at CAPITALONE-00348333 (memo following September 2009 meeting attended by Donald Trump, Jr. discussing financial troubles at 40 Wall); Ex. 322 at C117-119 (2013 supporting data reflecting Donald Trump, Jr.’s consultation on vacant space); Ex. 538 at TTO_01158462 (email reflecting Donald Trump, Jr.’s participation in a phone call in which Mr. Trump told a reporter in 2012 that 40 Wall Street had been appraised as being worth $600 million).

356. Moreover, after Mr. Trump became a federal official and his assets were placed into a revocable trust, Donald Trump, Jr. and Allen Weisselberg were the only two trustees of that trust. Ex. 521. The Statements of Financial Condition for the years ending June 30, 2016 and later purport to have been Donald Trump, Jr.’s responsibility, in addition to Mr. Weisselberg’s. As the June 30, 2016 statement articulates: “The Trustees of the Donald J. Trump Revocable Trust dated April 7, 2014, as amended, on behalf of Donald J. Trump are responsible for the accompanying statement of financial condition . . . .” Ex. 314 at MAZARS-NYAG-00001982. Statements to that effect are included on the Statements of Financial Condition from 2016 through 2020. E.g., Ex. 315 at MAZARS-NYAG-00001841; Ex. 316, Ex. 317, Ex. 318 at MAZARS-NYAG-00162247.

357. Donald Trump, Jr. also was directly involved in the loan transactions identified above. In particular, evidence obtained by the Attorney General establishes that he personally certified on an annual basis the truth and accuracy of the Statements of Financial Condition of Donald Trump to Deutsche Bank for 2016 through 2019.61 On some such certifications, Donald Trump, Jr. specified that he was doing so as “attorney in fact” for Donald J. Trump. Ex. 431 at DB-NYAG-059755 (certifying June 30, 2016 statement); Ex. 432 at DB-NYAG-210893 (certifying June 30, 2017 statement). In addition to those certifications, Donald Trump, Jr., signed other made representations concerning the financial performance of [individual properties] to Deutsche Bank in connection with those loans. Ex. 539 at DB-NYAG-026821 (certification of August 31, 2017 OPO financial statement); Ex. 540 at DB-NYAG-018107 (DSCR Certification as of December 31, 2017); Ex. 541 at DB-NYAG-266198 (certification of August 2018 OPO financial statement); Ex. 542 at DB-NYAG-407776 (certification of January 2019 OPO financial statement and DSCR); Ex. 543 at DB-NYAG-233879 (certification of August 2019 OPO financial statement and DSCR); Ex. 544 at DB-NYAG-407789 (certification of DSCR as of January 2020).

358. Beyond the Statements of Financial Condition and particular assets therein, documents obtained by the Attorney General establish that Donald Trump, Jr. received his own memoranda discussing the financial position of the Trump Organization as a general matter. There are multiple memoranda addressed to him enclosing spreadsheets which provided a “detailed financial analysis” on the business segments in the Trump portfolio. Ex. 545 at TTO_041325; Ex. 546 at TTO_041347; Ex. 547 at TTO_041326; Ex. 548 at TTO_658823; Ex. 549 at TTO_658601. The analyses contained projected cash flow figures, actual cash flow figures, and other data which would be relevant to the Statement of Financial Condition of Donald J. Trump. For example, the Statement of Financial Condition for 2017 includes cash in certain entities in which Mr. Trump is a minority limited partner in a figure reported as Mr. Trump’s own liquidity—but other internal documents sent to Donald Trump, Jr. reflected that any cash distributions from those entities were “at the discretion of” the general partner, not Mr. Trump. Compare Ex. 315 at MAZARS-NYAG-00001842 with Ex. 549.

III. Ivanka Trump Must Be Compelled to Testify359. Ivanka Trump began serving as an Executive Vice President in the Trump Organization in 2005. Ex. 330 at TTO_01751760. She left the Trump Organization in or around 2017.

360. While at the Trump Organization she “direct[ed] all areas of the company’s real estate and hotel management platforms.” Ex. 330 at TTO_01751760. This included active participation in all aspects of projects, “including deal evaluation, pre-development planning, financing, design, construction, sales and marketing” as well as “involve[ment] in all decisions— large and small.” Ex. 330 at TTO_01751760.

361. Ivanka Trump was the lead negotiator for the leasehold with the General Services Administration (GSA) for the Old Post Office Property. Ex. 550 at 9:02-10:22; Ex. 551 at TTO_03342133 at 15:21-16:04.

362. As part of that process, she submitted the Trump Organization’s proposal to the GSA in July 2011. Ex. 552 at TTO_02114052.

363. That proposal incorporated the Statement of Financial Condition of Donald J. Trump. Ex. 552 at TTO_02114204. (“Trump’s real estate investments are funded from Donald J. Trump’s significant net worth, which is composed of a wide range of capitalized affiliates. Please find Trump’s Statement of Financial Condition in an envelope submitted with each copy of this proposal.”).

364. The Trump Organization represented to the GSA that the Statement of Financial Condition was compiled under GAAP with any departures noted in the accountant’s compilation report. Ex. 552 at TTO_02114204.

365. While at the Trump Organization Ivanka Trump, along with Allen Weisselberg, was the primary point of contact for representatives of Deutsche Bank. Ex. 553 at 25:06-11.

366. As part of an ongoing search for financing on the Doral property, she was copied on a letter from Donald Trump to the CEO of Deutsche Bank Securities along with which he transmitted his Statement of Financial Condition and an additional letter meant to “establish [his] brand value.” Ex. 529 at TTO_214580.

367. Ms. Trump also discussed other, less favorable terms with respect to Doral with another financial institution for financing options not personally guaranteed by Mr. Trump. Ex. 554 at Beal 001652-53; Ex. 555 at BEAL001510; Ex. 556 at BEAL001511.

368. In the course of negotiating with Deutsche Bank financing for the Doral property, Ms. Trump was responsible for securing loan terms, which included a personal guaranty by Mr. Trump for which his representations regarding his financial condition would be (and were) made. Ex. 557 at DB-NYAG-012113. Deutsche Bank then issued a loan on Doral to Trump Endeavor LLC, an entity in the Trump Organization, and personally guaranteed by Mr. Trump. This loan (initially comprised of one secured tranche and one unsecured tranche) was for a total of $125 million and closed in June 2012. Ex. 368 at DB-NYAG-001693420; Ex. 356 at DB-NYAG- 004169.

369. An internal bank credit memorandum makes clear that the “Financial Strength of the Guarantor” (referring to Mr. Trump) and his personal guaranty were factors in favor of approving the loan. Ex. 368 at DB-NYAG-001693.

370. Following the Doral loan, Ivanka Trump was involved in negotiations regarding the Trump International Hotel and Tower Chicago.

371. As part of that transaction, she received term sheets from two different divisions of Deutsche Bank. Some term sheets included recourse through a personal guaranty while others did not. See Ex. 558 at TTO_01555089; Ex. 559 at TTO_01555090; Ex. 560 at TTO_01748494; Ex. 561 at TTO_01748497; Ex. 562 at TTO_01748510.

372. The bank’s internal credit memorandum, in recommending approval, noted the “unique nature” of the loans and stated that “the credit exposure is being recommended based on the financial profile of the Guarantor.” Ex. 424 at DB-NYAG-068526.

373. The final Chicago loans included a personal guaranty wherein it was represented that Mr. Trump’s June 30, 2012 Statement of Financial Condition was “true and correct in all material respects” and that the statement “presents fairly Guarantor’s financial condition as of June 30, 2012.” Ex. 364 at DB-NYAG-038878; Ex. 365 at DB-NYAG-003229.

374. After winning the bid to lease the Old Post Office, Ivanka Trump helped negotiate financing for the property. Ex. 563 at DB-NYAG-011630; Ex. 564 at DB-NYAG-011631. The personal guaranty for this loan required submission of Mr. Trump’s Statement of Financial Condition annually, along with a compliance certificate attesting that the statement presented fairly in all material respects Mr. Trump’s financial condition. Ex. 366 at DB-NYAG-003290-91, 3300-02.

375. In order to receive funds from Deutsche Bank, Ivanka Trump submitted several requisition draw requests. Ex. 565 at DB-NYAG-133282, -285, -290; Ex. 566 at DB-NYAG- 139707, -710, -715; Ex. 567 at DB-NYAG-129968, -9971, -9976; Ex. 568 at DB-NYAG- 140534, -537, -542; Ex. 569 at DB-NYAG-136544, -547, -552.

376. In her tenure at the Trump Organization, other employees would provide Ivanka Trump with financial analyses and projections relevant to the Statements and assets valued therein. Ex. 570 at 163:17-23; Ex. 545 at TTO_041325; Ex. 549 at TTO_658601.

377. One such analysis was an overall picture of the Trump Organization’s corporate cashflow prepared, in part, by Allen Weisselberg. Ex 545 at TTO_041325; Ex. 546 at TTO_041347; Ex. 549 at TTO_658601.

378. That analysis contained information on the operations of the “various business segments” in the Trump portfolio.

379. The information contained in the analysis which was prepared for internal use could provide insight into the valuations in the Statement of Financial Condition sent to lenders and insurers. For example, the golf club properties were valued using purported fixed assets in the financial statements rather than through the net operating income figures listed on the sheet. Many of those net operating income figures are below $1 million—while the clubs are valued in the tens or hundreds of millions—suggesting that the fixed assets approach could result in higher values for the golf clubs than a more typical income-based approach. Ex. 547 at TTO_041339.

380. Ivanka Trump’s Park Avenue Penthouse was incorporated into the valuation of the Trump Park Avenue asset on Donald Trump’s Statement of Financial Condition.

381. As discussed above, Ivanka Trump had an option to purchase a penthouse unit in Trump Park Avenue at $8,500,000. Ex. 394.

382. During the pendency of that option her unit was valued at between $12 million and $17 million higher than the option price. Ex. 380 at MAZARS-NYAG-00003290; Ex. 381 at MAZARS-NYAG-3476; Ex. 382 at MAZARS-NYAG-00000184.

383. When Ivanka Trump acquired a different option on another penthouse unit, that option price was reflected in the SOFC backup. Ex. 395 at TTO_02226839; Ex. 384 at MAZARS-NYAG-00000846.

CLAIM FOR RELIEF

Compelling Subpoena Compliance—C.P.L.R. § 2308384. The Attorney General repeats and realleges the preceding paragraphs as though fully set forth herein.

385. OAG’s subpoenas to respondents Donald J. Trump, Donald Trump, Jr., and Ivanka Trump dated December 1, 2021 (Exs. 301-303) were issued in a legally authorized investigation for which there is a sufficient factual basis, and the requests in the subpoenas are reasonably related to that investigation.

386. Respondents have not identified any legally cognizable basis for withholding from OAG any testimony, documents, or other communications responsive to OAG’s subpoenas.

387. Expedited briefing and resolution of OAG’s application to compel is necessary to prevent further unnecessary delay and interference with OAG’s investigation.

WHEREFORE, Petitioner respectfully requests that the Court grant the Supplemental Verified Petition in all respects and that a judgment and order be entered:

1. Compelling Donald J. Trump, within fourteen (14) days of the Court’s Order, to comply in full with that portion the OAG subpoena seeking documents and information, by producing all responsive records in his possession, custody and control, including but not limited to his documents held by the Trump Organization, and to certify such compliance in writing and under oath;

2. Compelling Donald J. Trump to testify pursuant to the OAG subpoena within twenty-one (21) days of certifying the completion of production of all documents, with every right to invoke the Fifth Amendment Privilege on the record in response to any specific question;

3. Compelling Ivanka Trump and Donald Trump, Jr. to testify pursuant to OAG’s subpoenas ad testificandum within twenty-one (21) days of the Court’s Order, with all Respondents being afforded every right to invoke the Fifth Amendment Privilege on the record in response to any specific question; and

4. For such further relief as this Court deems just and proper.

Dated: January 18, 2022

Respectfully submitted,

LETITIA JAMES

Attorney General of the State of New York

By: Austin Thompson (Signed)

Andrew Amer

Colleen K. Faherty

Alex Finkelstein

Wil Handley

Eric R. Haren

Louis M. Solomon

Austin Thompson

Stephanie Torre

Kevin Wallace

Office of the New York State Attorney General

28 Liberty Street

New York, NY 10005

Phone: (212) 416-8464

Austin.Thompson@ag.ny.govAttorneys for the People of the State of New York

VERIFICATIONAustin Thompson, An Attorney admitted to the Bar of this State, hereby affirms and certifies that:

I am an attorney in the Office of Letitia James, Attorney General of the State of New York, who appears on behalf of the People of the State of New York as Petitioner in this proceeding. I am duly authorized to make this verification and am acquainted with the facts in this matter.

I have read the annexed verified petition, know the contents thereof, and state that the same are true to my knowledge, except for those matters alleged to be upon information and belief, and as to those matters I believe them to be true.

Dated: New York, New York

January 18, 2022

Austin Thompson (Signed)

_______________

Notes:1 Citations to “Ex. __” are to true copies of the referenced documents as annexed to the Affirmation of Colleen Faherty, dated January 18, 2022, and filed with this petition. Certain exhibits to this Affirmation have been excerpted in order to avoid presenting the Court with extraneous material. As the parties requested, the Court has granted OAG leave to file exhibits under seal where they contain investigatory information. Docket No. 356.

2 From December 1995 to January 19, 2017, Mr. Trump was President of Seven Springs LLC. Seven Springs LLC is 99.9% owned by DJT Holdings LLC, an entity wholly owned by Mr. Trump until approximately 2016, when ownership was transferred to the Donald J. Trump Revocable Trust. Seven Springs LLC is 0.1% owned by Bedford Hills Corp., which was wholly owned by Mr. Trump until at least May 16, 2016, and is now wholly owned by DJT Holdings LLC. Ex. 331 at A4; Ex.332 at A2, A4; Ex. 333 at 4, A2; Ex. 334 at 00027709.12.2019.

3 Mr. Trump’s Statements of Financial Condition represent that valuations of Seven Springs were “based on an assessment made by Mr. Trump in conjunction with his associates . . . .” See, e.g., Ex. 312 (2012 Statement at 16).

4 The Statements of Financial Condition claim, among other things, that the valuations of the category “Club Facilities and Related Real Estate” were reached in an “assessment [that] was prepared by Mr. Trump working in conjunction with his associates and outside professionals.” Ex. 312 (2014 Statement at 8). See also Ex. 309 at MAZARS_NYAG_00003140; Ex. 307 at 8.

5 Donald Trump Testifies on Wind Turbines to the Scottish Parliament - April 25, 2012, at 01:47:31 - 01:47:58,

https://www.youtube.com/watch?v=HX4J1a8gy6I&t=6465s. Transcript available at

https://factba.se/transcript/donald-tru ... il-25-2017.

6 Values refer to the 71 mid-rise units as listed in the supporting data (Ex. 322 at rows 277-281; Ex.323 at rows 263-267; Ex. 324 at 265-269) unless otherwise noted.

7 Values refer to the 71 mid-rise units unless otherwise noted.

8 $55.1 million is a figure resulting from the percentage (76%) of a key valuation variable (effective gross revenue) attributable to income streams other than the building’s commercial units. Ex. 377 at TTO_234044, 055.

9 The appraisal also contained what is known as a “sum of gross sellout” of each unsold condominium unit using comparable properties totaling $164 million. Ex. 377 at TTO_234024-25, 56. The gross sellout figure determined the percentage of the loan collateral that was released if an unsold unit was sold to pay down the loan. Ex. 378 at TTO_03003564.

10 Before the sponsor of a condominium may offer units for sale, it is required to file an offering plan with the New York State Department of Law. GBL §352-e. The offering plan must, at a minimum, contain in detail the terms of the transaction and be complete, current, and accurate, and disclose all material facts relevant to a decision to purchase a unit, including the maximum price, as determined by sponsor, for units that are offered for sale. A sponsor may not offer units for sale at prices higher than those disclosed in the offering plan without first filing an amendment to the offering plan changing the maximum offering prices.

11 This practice may have occurred earlier. Jeff McConney testified that, when he was responsible for preparing the Statement of Financial Condition, he asked Trump International Realty for current market value figures on Trump Park Avenue. Ex. 388 at 745:04-17.

12 Blaise Cossalino v. The New York State Division of Housing and Community Renewal, Trump Park Avenue LLC, The Trump Corporation, NYSCEF Doc. 33 INDEX NO. 161368/2020 (Sup. Ct. N.Y. Cty.).

13 A Trump Organization Assistant Vice President, who evidence indicates had a substantial role in preparing the Statement of Financial Condition beginning with the June 30, 2016 statement, testified that he could “not recall a decision to change the practice to reporting current market value,” but that he probably “would have been instructed” to do so by Jeff McConney or Allen Weisselberg. Ex. 352 at 404:06-25.

14 In years from June 30, 2016 and later, “the Trustees” were referenced instead of “Mr. Trump,” but the references to “outside professionals” remained.

15 Such measures of liquidity can assist a bank in evaluating a borrower’s ability to repay a loan, including if the property that is collateral for the loan does not generate sufficient income to cover loan payments. Misrepresentations regarding a person’s liquidity may be actionable. See, e.g., Nairobi Holdings Limited v. Brown Brothers Harriman & Co., No. 02 CIV. 1230, 2002 WL 31027550, at *4-*5 (S.D.N.Y. Sept. 10, 2002) (misrepresentation regarding whether shortterm investment qualified as a “marketable security”).

16 This document is entitled “Agreement of Limited Partnership of Hudson Waterfront Associates I, L.P.” The partnership agreements for other pertinent entities—Hudson Waterfront Associates III LP, Hudson Waterfront Associates IV LV, and Hudson Waterfront Associates V LP—contain similar provisions. Without fully delineating the ownership structure, OAG understands that Vornado’s 70% stake in 1290 Avenue of the Americas and 555 California Street is owned directly or indirectly by means of these partnerships, and that Mr. Trump’s 30% stake is as well.

17 Donald J. Trump took part in extensive litigation regarding these partnerships in which control over partnership cash was addressed. See, e.g., Trump v. Cheng, 9 Misc. 3d 1120(A), at *7 (Sup. Ct. N.Y. Cty. Sept. 14, 2005) (quoting definition of “Cash Available for Distribution”).

18 This practice appears to have begun in 2013. See Ex. 399 (2012 schedule not including cash in or associated with Vornado properties).

19 For example, using the income capitalization approach, a property with a net operating income of $100 and a capitalization rate of 5% would yield a value of $2,000 (100/0.05).

20 The Statements of Financial Condition represent that the reported valuations of 40 Wall Street were based upon an evaluation by Mr. Trump working with others. See, e.g., Ex. 309 (2011 Statement at 7 (“The estimated current value of $524,700,000 is based upon a successful renegotiation of the ground lease and an evaluation made by Mr. Trump in conjunction with his associates and outside professionals . . . .”)); Ex. 310 (2012 Statement at 7 (similar)); Ex. 311 (2013 Statement at 7 (similar)).

21 Compare, e.g., Ex. 320 (2011 supporting data at row 118 (using $26.2 million net operating income figure, based on years of future projections)), with Ex. 408 at CAPITALONE- 00350719, -23 (2011 budget submitted to Capital One with $4.4 million figure); Ex. 321 (2012 supporting data at row 121 (using $22.72 million net operating income figure)) with Ex. 412 at CAPITALONE_00254432 (2013 projected budget sent to Capital One on December 13, 2012 subtracting expenses from receipts to arrive at “operating cash flow before debt service” of $14.3 million, accompanied by letter signed by Mr. McConney).

22 The term “Loan Document” included Mr. Trump’s guaranty and “any other document, agreement, consent, or instrument which has been or will be executed in connection with” the loan agreement and guaranty. Id. at 5865. The same conditions applied to the Chicago and OPO properties. Ex. 422 at DB-NYAG-006019, -6023; Ex. 423 at DB-NYAG-005307-12; Ex. 421 at DB-NYAG-005025, 5031.

23 Donald J. Trump, Eric Trump, Ivanka Trump, and Donald Trump, Jr. were officers and owners (directly or indirectly) of Trump Old Post Office LLC in 2014 approximately when Deutsche Bank extended credit in connection with that entity. Ex. 425 (at DB-NYAG-004655, - 656, -657, -678, -714.)

24 See Ex. 356 (Guaranty dated as of June 11, 2012 (Doral Guaranty)) at DB-NYAG- 004177-78; id. at 4173 (defining “Prior Financial Statements” to include Mr. Trump’s “Statement of Financial Condition, dated as of June 30, 2011”). The loan document expressly states that this representation was made “[i]n order to induce Lender to accept this Guaranty and to enter into the Credit Agreement and the transactions hereunder.” Id. at 4177-78.

25 Ex. 356 at 4188 (Mr. Trump’s signature).

26 Ex. 366 at DB-NYAG-003287. Evidence obtained by the Attorney General indicates that the Trump Organization obtained the Old Post Office loan proceeds in stages—with the last draws on the loan (totaling millions of dollars) occurring in 2017. Id. at Ex. 366.

27 Ex. 364 at DB-NYAG-038878 (Chicago residential portion guaranty); Ex. 365 at DBNYAG-003229 (Chicago hotel portion guaranty); Ex. 426 at DB-NYAG-003191 (amended and restated Chicago guaranty).

28 Ex. 346 at DB-NYAG-060415. For the June 30, 2015 statement, Trump Organization employees in May 2016 initially submitted a document signed by him certifying the June 30, 2014 statement, (see Ex. 427 at DB-NYAG-024830, Ex. 428 at DB-NYAG-024831), but soon corrected the error by submitting a corrected first page of the compliance certificate. Ex. 429 at DB-NYAG-015494; Ex. 430 at DB-NYAG-015495.

29 Ex. 431 at DB-NYAG-059755 (certifying June 30, 2016 statement); Ex. 432 at DBNYAG- 210893 (certifying June 30, 2017 statement); Ex. 433 at DB-NYAG-059824 (certifying June 30, 2018 statement); Ex. 434 at TTO_03595053 (certifying June 30, 2019 statement).

30 The individual Weisselberg was referring to was Douglas Larson, who left Cushman & Wakefield to join Newmark Group in June of 2017.

31 This last estimate clearly conflicted with the December 10 costs of $10,099,165. See Ex. 460 at 798355.

32 Despite commissioning this appraisal concluding based on financial performance and sales comparisons that the property as a golf course was worth either $15 million or $16 million (with and without the driving range), see Ex. 466 at MLB_EM00005562-63, supporting data for Mr. Trump’s Statement of Financial Condition for the year ending June 30, 3014 asserted that the golf club at the property was worth $74.3 million—comprised of “fixed assets” and the brand premium described supra at ¶¶ 80-98. See, e.g., Ex. 324 at rows 383-386.

33 The 2008 Draft Environmental Impact Statement prepared by environmental consultants retained by the Trump Organization states: “No development is currently proposed in the New Castle portion of the site.” Ex. 486 at II-70 (item J). The 2008 DEIS analyzed these issues “for informational and cumulative impact analysis purposes only.” Id. The DEIS noted that five single-family homes could be developed on the New Castle portion of the site “utilizing existing zoning and given existing environmental constraints,” but noted that because access for such homes “would be from the terminus of Oregon Road (north) at the New Castle/Bedford town line with an additional 1,230 linear feet of roadway, ending in a cul-de-sac,” any such development “would violate the Bedford Land Subdivision Regulations regarding the maximum number of lots permitted on a dead-end street.” Id. (noting that “[t]here would be no access to Sarles Street,” referring to access exiting to the west of the Seven Springs parcel).

34 Even absent such direct testimony of Mr. Trump’s involvement, knowledge of Mr. Trump’s agents presumptively would be imputed to him as a matter of law in civil litigation. See, e.g., Kirschner v. KPMG LLP, 15 N.Y.3d 446, 465 (2010) (“Agency law presumes imputation even where the agent acts less than admirably, exhibits poor business judgment, or commits fraud.”).

35 The complaint in Trump v. Vance cited many of the same statements now points to in the Motion. Compare Docket No. 354 at 3-4 with Trump v. Vance, 19 Civ. 8694, Docket No. 1 at ¶ 38.

36 Another document is a two-page document entitled “The Donald J. Trump Revocable Trust” in which the two pages are labeled “Page 1 of 46” and “Page 46 of 46.” Ex. 526. This document contains Mr. Trump’s signature and is dated April 7, 2014 (the date OAG understands was the trust’s inception date) and reflects that the trustee of the trust “shall pay such part or all of the net income or principal of the trust to me as I may direct from time to time.” Id. at 545.

37 Exs. 304-319.

38 The assets included therein include, for example, assets with which Mr. Trump has publicly associated himself—such as his own triplex apartment in Trump Tower in New York, NY; Trump Tower; the Mar-a-Lago social club in Palm Beach, Florida; and many other properties that colloquially considered part of the Trump Organization.

39 Evidence obtained by the Attorney General to date indicates that an Assistant Vice President at the Trump Organization became a principal participant in the creation of the Statements of Financial Condition approximately in November 2016. Ex. 352 at 177.

40 Ex. 337 at 82:3-83:14.

41 Id. at 83:4-14.

42 Ex. 357 at 140:21-141:24.

43 Ex. 527 at 589:03-08, 607:03-13, 627:06-16, 671:03-08, 697:08-698:02.

44 Evidence obtained by the Attorney General also suggests that Donald J. Trump had awareness of the financial picture of the Trump Organization. A memo dated October 15, 2016 and addressed to Mr. Trump reads, “per your request enclosed please find a detailed analysis setting forth our various business segments and their resulting operations.” Ex. 528 at TTO_658594. The financial performance of Trump Organization businesses is a matter relevant to their value.

45 See Ex. 356 (Guaranty dated as of June 11, 2012 (Doral Guaranty) DB-NYAG- 004169), at 4178004177; id. at 4173 (defining “Prior Financial Statements” to include Mr. Trump’s “Statement of Financial Condition, dated as of June 30, 2011”). The loan document expressly states that this representation was made “[i]n order to induce Lender to accept this Guaranty and to enter into the Credit Agreement and the transactions hereunder.” Id. at 4177-78.

46 Id. at 4188 (Mr. Trump’s signature)

47 Ex. 366 at DB-NYAG-003287. Evidence obtained by the Attorney General indicates that the Trump Organization obtained the Old Post Office loan proceeds in stages—with the last draw on the loan (totaling millions of dollars) occurring in 2017. [EH-18] at DB-NYAG-217183.

48 Ex. 364 at DB-NYAG-038878 (Chicago residential portion guaranty); Ex. 365 at DBNYAG-003229 (Chicago hotel portion guaranty); Ex. 426 at DB-NYAG-003191 (amended and restated Chicago guaranty).

49 Ex. 346 at DB-NYAG-060415. For the June 30, 2015 statement, Trump Organization employees in May 2016 initially submitted a document signed by him certifying the June 30, 2014 statement (Ex. 427 at DB-NYAG-024830, Ex. 428 at DB-NYAG-024831) but soon corrected the error by submitting a corrected first page of the compliance certificate (Ex. 429 at DB-NYAG-015494, Ex. 430 at DB-NYAG-015495).

50 The term “Loan Document” included Mr. Trump’s guaranty and “any other document, agreement, consent, or instrument which has been or will be executed in connection with” the loan agreement and guaranty. Id. at 5865. The same conditions applied to the Chicago and OPO properties. Ex. 422 at DB-NYAG-006019, -6023; Ex. 423 at DB-NYAG-005307-12; Ex. 421 at DB-NYAG-005025, 5031.

51 Ex. 529; Ex.533; Ex. 534.

52 See, e.g., Ashley Parker and Philip Rucker, Donald Trump waits in his tower — accessible yet isolated, Washington Post, January 17, 2017 (“He does not use email and rarely surfs the Internet, meaning that telephone calls, television appearances or physical proximity are the best ways to reach him.”); Ex. 531 at 316:09-316:10 (“Well, he doesn’t use e-mail, so there – so there is no e-mail.”)

53 See Ex. 531 at 310:09-310:24 (file cabinets containing DJT documents); 312:24-313:10 (assistant holding documents); 316:03-316:17 (DJT correspondence file); 318:09-318:21 (communication by Post-It Note).

54 Ex. 312 (2015 Statement of Financial Condition at MAZARS-NYAG-00000688.).

55 McConney Tr. at 82 (“Prior to November of ‘16, once all the information was provided to Bender’s firm, Bender would produce a paper document, a draft document, and Allen Weisselberg I believe reviewed it with Mr. Trump. So I would go through the paper document. Allen would go through it to see if there's any typos or any corrections or make sure everything was -- the interest rates were correct or whatever. But I believe Allen spoke with Mr. Trump about something with the statement.”); McConney Tr. at 98 (“He would review it with Allen as the final review, I guess you would call it. But that’s what I know about that.”).

56 See Ex. 529 at TTO_214580; Ex. 533 at TTO_214579; Ex. 534 at TTO_214581.

57 Ex. 529 at TTO_214580

58 Ex. 535 at TTO_122958

59 Ex. 536 at TTO_122961

60 Ex. 505, at 13:3-16:15. Even absent such direct testimony of Mr. Trump’s involvement, knowledge of Mr. Trump’s agents presumptively would be imputed to him as a matter of law in civil litigation. See, e.g., Kirschner v. KPMG LLP, 15 N.Y.3d 446, 465 (2010) (“Agency law presumes imputation even where the agent acts less than admirably, exhibits poor business judgment, or commits fraud.”).

61 Ex. 431 (certifying June 30, 2016 statement); Ex. 432 (certifying June 30, 2017 statement); Ex. 433 (certifying June 30, 2018 statement); Ex. 434 (certifying June 30, 2019 statement).